South Mediterranean tourism shows 59% summer dependence | News

_destinationMain_1534851250762-300x0.jpg)

A new report by Data Appeal Mabrian (Almawave/Almaviva Group), highlights how European destinations can strategically boost low-season demand by expanding and diversifying their offerings beyond traditional peak periods, signalling the need for a coordinated shift in how destinations design and promote year-round travel experiences.

The study, presented by Emilio Inés, Tourism Global Director at The Data Appeal Company at the Seasonality Summit 2026 in Rimini, analyses low-season inbound demand trends across Italy, Spain, Greece, Croatia and Portugal within the South Mediterranean context. It examines seasonality patterns, traveller profiles, air connectivity, pricing trends and demand drivers across key Southern European destinations, providing strategic insights to support the development of more balanced year-round tourism models.

Key findings show that destinations are progressing at different speeds in addressing seasonality. According to the Summer Dependence Rate*, Spain records the lowest peak-season dependence (52.8%), well below the South Mediterranean average of 59.1%, followed by Portugal (54.5%) and Italy (58.7%). By contrast, Greece (72.9%) and Croatia (79.1%) remain significantly more reliant on summer demand, although Greece is showing early signs of extending tourism activity into the shoulder seasons.

The report identifies distinct low-season traveller profiles. From January to March, demand is largely driven by couples from nearby markets in midscale accommodation; whereas October to December sees a shift towards established European markets, with travellers more likely to extend summer and opt for upscale hotels.

According to the analysis, in-destination events are also playing a key role in driving low-season demand. As Emilio Inés noted at the Seasonality Summit: “Organically counter-seasonal, between 53% and 72% of events already take place outside peak months, while 58% to 73% of total attendance is concentrated in the low season, effectively turning events into a demand powerhouse for low season periods.”

Connectivity, Climate, Pricing and Experiences: Key Levers for Seasonality Mitigation

The report highlights that improving low-season performance requires a deeper understanding of traveller motivations, better alignment between event calendars and tourism products, and stronger targeting of high-connectivity source markets. Climate perception, pricing advantages and curated experiences are identified as key levers to redistribute demand more evenly throughout the year.

Air connectivity across the five destinations studied is set to expand further in late 2026. Between October and December 2026, a total of 96.64 million seats will connect Italy, Spain, Greece, Croatia and Portugal, representing a +4.6% increase compared with the same period in 2025. All destinations are expected to record growth in Q4 2026 except Portugal (-2.5%). Greece leads expansion with +10.7%, followed by Spain (+5.4%) and Italy (+4.2%).

According to the Data Appeal expert, “leveraging inbound markets with increasing low-season connectivity is essential, alongside strengthening airline networks that extend beyond peak months.” This includes both low-cost carriers—particularly relevant in Italy and Spain—and traditional airlines, which are expanding seat capacity in the low season across Italy, Spain and Greece. In Croatia and Portugal, low-season connectivity accounts for an average of 58.5% of total capacity.

The report identifies climate perception as a growing competitive advantage for low season travel, particularly among short- and medium-haul repeat visitors, as well as flexible segments such as young adults, digital nomads and senior travellers. Based on the Perception of Climate Index (PCI), the study unveils “windows of climate opportunity” when actual weather conditions exceed traveller expectations. Italy, Spain and Greece typically show two such windows—late winter/early spring and autumn—while Croatia and Portugal benefit from an additional spring window.

“When aligned with inbound holiday calendars, these periods present significant opportunities to stimulate low-season demand,” highlights Data Appeal’s Tourism Global Director. Data indicates that the UK, Germany and France represent a structural base for low season travel, with 63%, 60% and 53% of holidays respectively taking place outside peak periods.

Pricing also plays a key role in shaping demand. In winter 2026, hotel rates across the destinations analysed are significantly lower than in summer 2025, with average reductions of 24.6% for 3-star hotels, 22.4% for 4-star hotels, and close to one-third for 5-star properties.

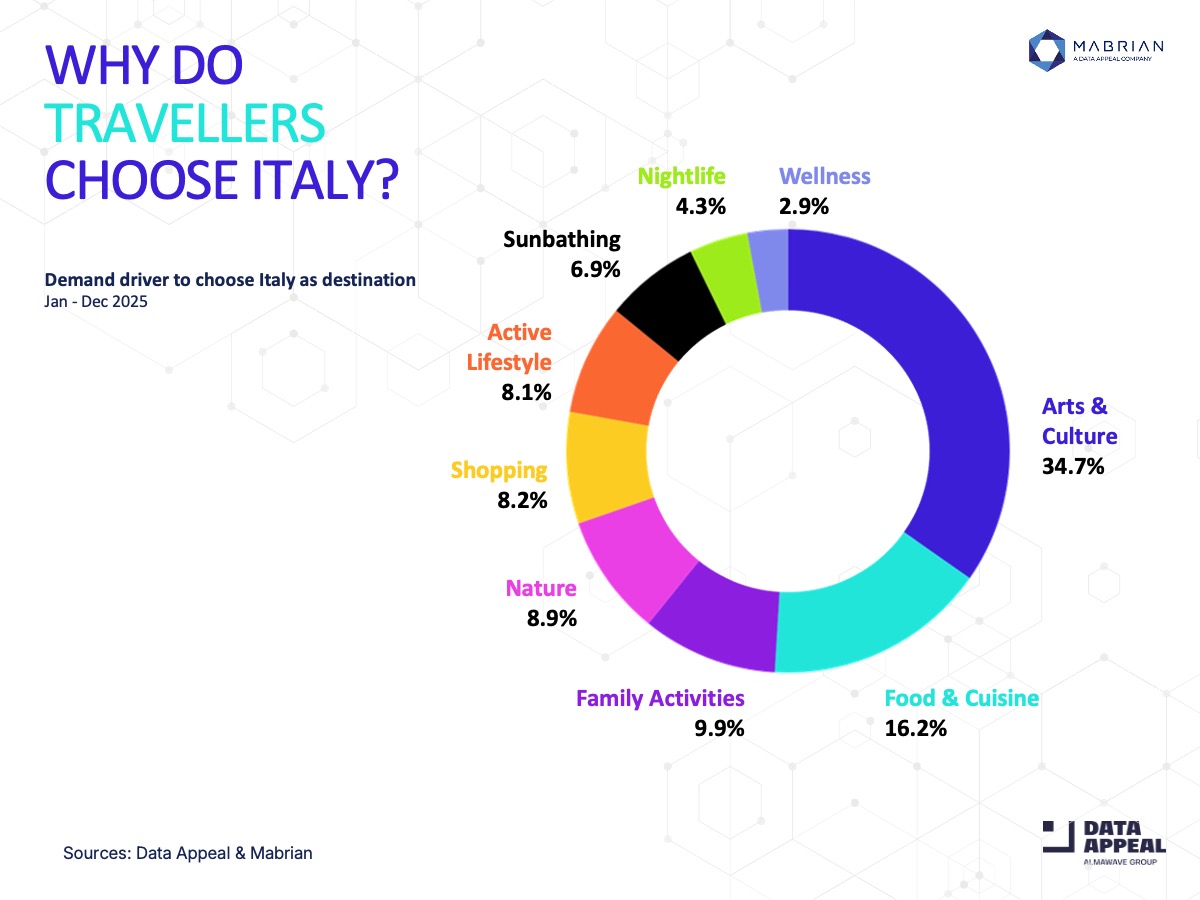

Finally, the report highlights that many of the most engaging tourism activities for travellers visiting the studied European destinations—including cultural, nature-based, gastronomy and active experiences—are inherently less seasonal and highly adaptable throughout the year, offering strong potential to further redistribute demand beyond peak periods.

* Summer Dependance Rate: Proprietary indicator that measures the concentration of tourist activity during the summer period. It represents the percentage of total annual tourism activity — based on reviews from verified and completed accommodation stays — that occurs between May and September (inclusive), relative to overall year-round activity.